Er zijn meer dan 400.000 verzekeringsagenten in dit land, en bijna allemaal willen ze u graag een volledige levensverzekering verkopen. Als u een polis koopt met een premie van €40.000 per jaar, ligt de commissie doorgaans ergens tussen de €20.000 en €44.000 voor die makelaar. Zoals u zich misschien kunt voorstellen, kan die commissie zeer motiverend zijn, vooral gezien het gemiddelde inkomen van verzekeringsagenten van $ 49.840. Tot overmaat van ramp bieden veel van de slechtste polissen de hoogste commissies. Helaas wordt de overgrote meerderheid van de verkochte polissen op ongepaste wijze verkocht en zijn de overgrote meerderheid van degenen die deze polissen verkopen verkopers die zich voordoen als financiële adviseurs.

Als gevolg van dit belachelijke belangenconflict kunnen agenten vaak een aantal serieuze mythes naar buiten gooien in een poging je ervan te overtuigen hun product te kopen, wat de vernietigende statistiek zou kunnen verklaren dat meer dan 80% van degenen die dit product kopen het vóór de dood kwijtraken. Uit opiniepeilingen onder echte artsen op deze site en onze Facebook-groep blijkt dat de overgrote meerderheid van degenen die een levenslange polis hebben gekocht, spijt heeft van hun aankoop. Als dit allemaal nieuws voor je is, lees dan Alles wat je moet weten over levensverzekeringen voordat je verder gaat met dit bericht.

Hoewel de meeste WCI FB-groepsleden nog nooit een volledige levensverzekering hebben afgesloten, heeft 76% van degenen die dat wel hebben gedaan er spijt van.

Laden ...

De cijfers zijn vergelijkbaar, maar iets lager in de lopende enquête op deze site (die in tegenstelling tot de FB-groep toestaat dat degenen die deze polissen verkopen, stemmen).

Veel mensen denken dat ik een hekel heb aan levensverzekeringen. Eigenlijk niet. Ik haat de manier waarop het wordt verkocht en degenen die het op ongepaste wijze verkopen. Als je echt begrijpt hoe het werkt en het nog steeds wilt, koop dan gerust zoveel als je wilt. Het raakt mij op de een of andere manier eigenlijk niet. Maar ik ben het beu om lezers en luisteraars tegen te komen die NIET begrepen hoe het werkte toen ze het kochten, en als ze het eenmaal begrijpen, WILLEN het NIET.

Een Levensverzekering kan op veel verschillende manieren worden afgesloten, maar over het algemeen betaalt u een maandelijkse of jaarlijkse premie voor een bepaalde periode of tot u overlijdt. Hoe langer de periode waarover u de premie betaalt, hoe lager de premie. Wanneer u overlijdt, krijgt uw begunstigde de opbrengst van de polis. Omdat elke levensverzekering gegarandeerd uitkeert als u deze tot aan uw overlijden vasthoudt, zijn de premies veel hoger dan bij een vergelijkbare overlijdensrisicoverzekering.

Een volledige levensverzekering is, net als andere vormen van permanente levensverzekeringen, eigenlijk een hybride van verzekering en beleggen. Het beleid accumuleert contante waarde naarmate de jaren verstrijken. Die contante waarde groeit op een fiscaal beschermde manier, en je kunt het geld daar zelfs belastingvrij (maar niet rentevrij) lenen. Bij uw overlijden wordt het geleende bedrag (plus de rente) van de overlijdensuitkering afgetrokken en wordt de rest aan uw begunstigde betaald. (U krijgt de contante waarde of de uitkering bij overlijden, niet beide.)

Door dit beleggingsaspect kunnen degenen die volledige levensverzekeringen verkopen allerlei creatieve redenen vinden waarom u deze zou moeten kopen en creatieve manieren om deze te structureren. De meest extreme voorstanders kunnen zelfs beweren dat je gedurende je hele leven GEEN ENKEL ander financieel product nodig hebt, omdat een levensverzekering blijkbaar in al je behoeften kan voorzien, inclusief hypotheken, consumentenleningen, verzekeringen, beleggingen, studiesparen en pensioen.

Het probleem is dat er voor elk gebruik van een volledige levensverzekering meestal een betere manier is om met dat financiële probleem om te gaan. Dit bericht bevat de 38 veelvoorkomende mythen over levensverzekeringen die door de voorstanders ervan worden gepropageerd.

Een volledige levensverzekering is niet de beste manier om uw inkomen te beschermen; een overlijdensrisicoverzekering is dat wel. Voordat u met pensioen gaat, kunt u een goedkope overlijdensrisicoverzekering afsluiten om voor uw dierbaren te zorgen als u voortijdig overlijdt. Een levensverzekeringspolis met een looptijd van 30 jaar en een nominale waarde van $1 miljoen, gekocht voor een gezonde 30-jarige, kost $680 per jaar. Een soortgelijke levenslange polis zal meer dan tien keer zoveel kosten, $8.000-$10.000 per jaar. Dat is geld dat niet kan worden besteed aan hypotheekbetalingen of vakanties, en ook niet kan worden belegd voor pensioen.

Het hele leven is niet de beste manier om een permanente uitkering bij overlijden te krijgen; het gegarandeerde, universele leven is dat wel. Er zijn een select aantal mensen die een verzekering nodig hebben of willen die uitkeert bij hun overlijden, wanneer dat ook mag zijn. Dit kan handig zijn bij ongebruikelijke kwesties op het gebied van vermogensplanning. Er is echter een beter product dat dit biedt en dat veel goedkoper is dan een volledige levensverzekering. Het heet Gegarandeerde universele levensverzekering zonder verval . Het accumuleert GEEN contante waarde, maar biedt eenvoudigweg een levenslange uitkering bij overlijden. Het kost slechts de helft van de totale levensverzekering, dus het zal u niet verbazen dat de commissie van de makelaar op deze verkoop veel lager zal zijn.

Noem mij cynisch, maar ik vermoed dat dit een van de redenen kan zijn waarom je nog nooit hebt gehoord van gegarandeerd universeel leven zonder verval. Een volledige levensverzekering biedt een gegarandeerde uitkering bij overlijden die naar verwachting (maar niet gegarandeerd) langzaam zal groeien, zodat als u overlijdt op uw levensverwachting of later, u iets meer achterlaat dan de oorspronkelijke uitkering bij overlijden.

Een levenslange polis waar ik onlangs naar keek voorspelde dat de overlijdensuitkering van een polis van $1 miljoen, gekocht op 30-jarige leeftijd, $3,17 miljoen zou zijn bij overlijden op 83-jarige leeftijd. Dat klinkt geweldig, bijna als een inflatiebescherming van de overlijdensuitkering. Behalve dat de historische inflatie ongeveer 3,1% bedraagt. Met 3,1% zou $1 miljoen nu het equivalent zijn van $5,04 miljoen over 53 jaar. Een beleid voor het hele leven zou verwoest worden door onverwachte inflatie, aangezien de dividenden voornamelijk worden gedekt door nominale obligaties, waarvan de waarden zouden worden vermoord in een klimaat van hoge inflatie.

Daarom is een volledige levensverzekering noch de beste manier om een gegarandeerde levenslange nominale overlijdensuitkering, noch een gegarandeerde levenslange reële overlijdensuitkering te bieden. Dus waar is het goed voor? Hoe zit het met een gegarandeerde overlijdensuitkering die zou kunnen stijgen als de verzekeringsmaatschappij zin heeft om deze te verhogen? Bent u bereid daarvoor een twee keer zo hoge premie te betalen? Dat dacht ik niet.

Het hele leven is niet de beste manier om te beleggen; traditionele beleggingen zijn dat wel. Wanneer u uw hele levenspremie betaalt, gaat een deel van het geld naar de aanschaf van een verzekering, een deel ervan gaat naar overhead en winst voor de verzekeringsmaatschappij, en een deel ervan gaat naar de commissie voor de verkoper. De rest gaat vervolgens naar het contante waardegedeelte van de polis.

Elk jaar declareert de verzekeringsmaatschappij een dividend, en als er €10.000 in het contante waardegedeelte zit en het dividend 6% bedraagt, wordt €600 bijgeschreven op uw contante waarde. Het dividend wordt alleen toegepast op de contante waarde, niet op de volledige betaalde premie, dus het gemiddelde dividendpercentage is op geen enkele manier, vorm of vorm gerelateerd aan uw daadwerkelijke rendement op de polis als belegging. In feite is het rendement op investeringen over het algemeen minstens tien jaar negatief. Ik heb onlangs een beleid geanalyseerd voor een gezonde 30-jarige man met een levensverwachting van 53 jaar. Het gegarandeerde rendement op de contante waarde was minder dan 2% per jaar NA 5 DECENNIA .

Zelfs als u de optimistische “geprojecteerde” waarden van de verzekeringsmaatschappij gebruikt, ziet u nog steeds een rendement van minder dan 5%. In werkelijkheid kom je waarschijnlijk uit op een rendement van 3%-4%. Als je bedenkt dat je deze “investering” vijf decennia lang moet vasthouden, lijkt dat niet veel compensatie. Als u tientallen jaren de tijd heeft om te beleggen, is het veel verstandiger om meer risico te nemen met uw beleggingen en een hoger rendement te behalen. Een belegging in aandelen of onroerend goed levert over tientallen jaren waarschijnlijk een rendement op tussen de 7% en 12%. $100.000, geïnvesteerd gedurende 50 jaar tegen 3% per jaar, zal uitgroeien tot $438.000. Als het in plaats daarvan met 9% groeit, krijg je $7,4 miljoen, of 17 keer zoveel geld. De snelheid waarmee u uw langetermijninvesteringen samenstelt, is van belang, vooral over langere perioden.

Sommige agenten zijn van mening dat verzekeringsmaatschappijen op de een of andere manier beleggingsrendementen kunnen krijgen die u of ik elders niet kunnen vinden, en dat geweldige rendement kunnen doorgeven aan hun polishouders. Het kan verhelderend zijn om onder de motorkap te kijken en te zien wat er werkelijk in de portefeuille van een verzekeringsmaatschappij zit. In 2016 werden de activa van verzekeringsmaatschappijen voor 67% belegd in obligaties (bijna allemaal in gewone bedrijfsobligaties en staatsobligaties), 1% in preferente aandelen, 12% in gewone aandelen, 8% in hypotheken, 1% in onroerend goed, 4% in contanten, 2% in leningen aan hun polishouders en ongeveer 5% in ‘andere’. Dankzij de indexfondsrevolutie kan een individuele belegger bijna al dat spul kopen voor minder dan 10 basispunten per jaar aan kosten. Actief beheer werkt niet beter voor verzekeringsmaatschappijen dan voor beleggingsfondsen.

Zoals je zou verwachten, zijn de rendementen op een portefeuille die voornamelijk bestaat uit staatsobligaties (momenteel 1%-2%) en bedrijfsobligaties (momenteel 3%-4%) niet bijzonder hoog. Waar komen dividenden dan vandaan? Een deel komt van het rendement op de beleggingsportefeuille, een deel komt van de vergoedingen van degenen die hun polis hebben afgestaan, en een deel komt van ‘sterftekredieten’, wat in feite geld is dat ze niet aan de begunstigden hoefden uit te betalen omdat er minder mensen stierven dan ze hadden gepland (dat wil zeggen, je hebt in de eerste plaats te veel betaald voor het verzekeringsgedeelte van de polis vanwege overheidsregels). Er zijn geen magische investeringen waarin verzekeringsmaatschappijen kunnen investeren die u niet zonder het bedrijf kunt doen. Elke extra laag tussen u en de investering verhoogt alleen maar de kosten en verlaagt het rendement.

Er zijn veel activaklassen die de moeite waard zijn om in een gediversifieerde portefeuille op te nemen, maar het hele leven is daar niet één van. Verzekeringsverkopers nemen meestal hun toevlucht tot dit argument zodra ze zich realiseren dat ze je er niet van kunnen overtuigen dat het hele leven op zichzelf een grote investering is. Ze zeggen dat als je het mengt in een portefeuille van aandelen, obligaties en onroerend goed, dit de algehele portefeuille zal verbeteren. U kunt echter alles wat u maar wilt een beleggingscategorie noemen. Paardenmest kan een beleggingscategorie zijn, maar dat betekent niet dat u erin moet beleggen. Denk er zo over na. Als ik je vertelde dat ik een beleggingscategorie had met de volgende kenmerken:

zou jij het kopen? Natuurlijk niet.

Het hele leven is niet de beste manier om uw investeringsbelasting te verlagen, pensioenrekeningen wel. Veel agenten willen graag de belastingvoordelen van een volledige levensverzekering aanprijzen, waarbij ze deze vaak vergelijken met een 401 (k) of een Roth IRA. De contante waarde groeit op een fiscaal beschermde manier, de contante waarde kan belastingvrij worden geleend en de opbrengsten van de polis bij uw overlijden zijn inkomsten (hoewel geen nalatenschap) belastingvrij. Sommige voorstanders van het hele leven suggereren dus dat je een volledige levensverzekering gebruikt in plaats van een pensioenrekening zoals een 401 (k) of een Roth IRA. Een 401(k) of Roth IRA levert echter niet alleen MEER belastingbesparingen op en stelt u in staat te investeren in risicovollere beleggingen die u waarschijnlijk een hoger rendement zullen opleveren, maar u hoeft ook niet uw eigen geld te lenen, noch rente te betalen voor het voorrecht om dit te doen.

Ik heb eerder gepost over de 3 manieren waarop een 401(k) u op belastingen bespaart en over hoe een hele levensverzekering niet op een Roth IRA lijkt. Ik heb ook gepost over hoe fiscaal-efficiënte beleggingen in een belastbare beleggingsrekening lang niet zoveel belastingdruk met zich meebrengen als agenten u graag vertellen dat ze dat wel doen. Zijn er fiscale voordelen verbonden aan het beleggen in levensverzekeringen? Ja, maar ze zijn dramatisch oververkocht.

Verzekeringsagenten gebruiken deze graag tegen artsen, die paranoïde kunnen zijn over kwesties met betrekking tot vermogensbescherming. Ze vermelden echter vaak niet (of weten misschien zelfs niet) dat de wetten ter bescherming van activa zeer staatsspecifiek zijn. Bijvoorbeeld [2022] In Alabama wordt slechts $ 500 aan contante waarde van een levensverzekering beschermd tegen schuldeisers, maar 100% van het geld in uw 401 (k) of IRA is beschermd. West Virginia biedt slechts een bescherming van $ 8.000. South Carolina beschermt $ 4.000. New Hampshire biedt geen enkele bescherming. Veel staten bieden 100% bescherming voor de contante waarde van levensverzekeringen, maar u moet waarschijnlijk de specifieke wetten van uw staat opzoeken voordat u in deze mythe trapt.

Levensverzekeringen met contante waarde hebben een aantal geweldige functies voor vermogensplanning die erg nuttig kunnen zijn. De overgrote meerderheid van de mensen, inclusief artsen, heeft deze functies echter niet nodig. Het belangrijkste voordeel van een levensverzekering is dat u bij uw overlijden een hoop inkomstenbelastingvrij geld krijgt. Dit kan helpen bij veel liquiditeitsproblemen, zoals het bezit van duur onroerend goed of een privébedrijf. Als u twee kinderen heeft die u gelijkelijk in uw nalatenschap wilt delen, en het grootste deel van uw nalatenschap bestaat uit de familieboerderij, dan zouden zij de boerderij moeten verkopen, in tweeën moeten knippen of de een de ander moeten laten uitkopen om gelijkelijk te kunnen delen. Als u echter ook een levensverzekering had met dezelfde waarde als de boerderij, kon het ene kind de boerderij krijgen en het andere kind de verzekeringsopbrengsten. Op dezelfde manier, in het gelukkige geval dat u een zeer groot landgoed heeft (meer dan $ 5 miljoen voor alleenstaanden in de federale belastingwet, maar in sommige staten kan dit veel minder zijn), kunnen de opbrengsten uit de levensverzekering worden gebruikt om de successierechten te betalen. Dit zou zelfs handig zijn als er maar één erfgenaam is, om te voorkomen dat hij een waardevol bezit of bedrijf tegen verkoopprijzen verkoopt om de belastingaanslag te betalen.

Sommige mensen houden er ook van om levensverzekeringen in een onherroepelijk vertrouwen te plaatsen om de omvang van hun nalatenschap te verkleinen en successierechten te vermijden. Hoewel u in plaats daarvan eenvoudige belastbare investeringen in de trust kunt stoppen (en waarschijnlijk hoger uit de bus komt vanwege hogere rendementen), kunnen de belastingtarieven voor trusts behoorlijk hoog zijn, waardoor de rendementen voor fiscaal inefficiënte investeringen ernstig worden ondermijnd, om nog maar te zwijgen van de gedoefactor. Het is belangrijk om erop te wijzen dat het niet de levensverzekering is die geld bespaart op successierechten, maar het feit dat u uw bezittingen weggeeft voordat u overlijdt door ze in de trust te stoppen.

Feit is echter dat de overgrote meerderheid van de Amerikanen, zelfs artsen, en zelfs artsen met een 'vermogensbelastingprobleem', geen volledige levensverzekering nodig hebben om aan effectieve vermogensplanning te kunnen doen. De meeste mensen zullen sterven zonder enige successierechten. Van degenen wier landgoederen enige successierechten verschuldigd zijn, beschikt de overgrote meerderheid over liquide middelen die kunnen worden gebruikt om de belastingen te betalen. Zelfs als u de omvang van uw nalatenschap wilt verkleinen om successierechten te voorkomen, kunt u dit eenvoudig doen zonder een levensverzekering af te sluiten. Jij en je partner kunnen elk $ 16.000 schenken [2022 – bezoek onze pagina met jaarcijfers voor de meest actuele cijfers] aan een erfgenaam in een bepaald jaar, zonder gevolgen voor de successie-/schenkbelasting. Als u bijvoorbeeld vier kinderen had en zij hadden elk vier kinderen en alle twintig erfgenamen waren getrouwd, dan zijn dat veertig mensen. 40 x $16.000 x 2 =$1,28 miljoen per jaar, dat uit uw nalatenschap kan worden gehaald zonder dat u successierechten/schenkbelasting hoeft te betalen. Het zal niet lang duren om met dat tarief onder de limiet van de successierechten te komen, er is geen verzekering nodig.

Sommige agenten gaan zelfs zo ver dat ze suggereren dat je een levenslange polis gebruikt om de studie van je kinderen te betalen. Kun jij dit? Natuurlijk. Je sluit gewoon een polislening af en stuurt dat geld naar de universiteit om het collegegeld te betalen. Maar je kunt om meerdere redenen beter sparen voor de universiteit met een goede 529. Ten eerste krijgt u vaak een belastingvoordeel van de staat door een 529 te gebruiken die niet beschikbaar is voor een volledige levensverzekering. Ten tweede hoeft u geen geld te lenen van uw 529, u neemt het gewoon op. Geen rentebetalingen vereist. Als laatste, maar zeker niet als minste, moet u rekening houden met het tijdsbestek van het sparen voor uw studie. Ouders sparen over het algemeen gedurende een periode van 5 tot 20 jaar voor hun studie. Door dat geld agressief te beleggen, kunnen ze een rendement van 7%-10% verwachten. Volledige levensverzekeringen hebben zeer slechte rendementen voor perioden van minder dan 20 jaar. In feite is het rendement op uw ‘investering’ in uw hele leven vaak negatief gedurende minstens tien jaar. Het is belangrijk om ervoor te zorgen dat uw geld net zo hard werkt als u, en dat uw geld de eerste tien jaar van uw levenspolis op vakantie is. Voorstanders van het hele leven zullen erop wijzen dat als je overlijdt, de uitkering bij overlijden nog steeds de studie van Junior kan betalen, maar het is veel goedkoper om dat risico te dekken met een overlijdensrisicoverzekering.

Verzekeringsagenten zullen af en toe op dit argument teruggrijpen als erop wordt gewezen dat een cliënt eigenlijk geen enkele behoefte heeft aan een permanente uitkering bij overlijden. Ze geven toe dat de klant eigenlijk geen volledige levensverzekering nodig heeft. Vervolgens proberen ze het te verkopen op basis van het feit dat het een statussymbool of luxe is. “Tuurlijk, je hebt het niet nodig, het is een luxe.” Een luxe is per definitie iets wat je niet nodig hebt. Ik geef er de voorkeur aan dat mijn luxe iets is waar ik echt van geniet. Dus voordat u als luxe een volledige levensverzekering aanschaft, moet u zich de vraag stellen:“Waar geniet ik echt van?” Als het een volledige levensverzekering heeft, prima, koop er dan een paar. Maar ik durf te wedden dat de meesten van ons de voorkeur geven aan luxe, zoals een mooie auto, een cruise met de kleinkinderen, of misschien een donatie aan een favoriet goed doel.

Het hele leven is niet de beste manier om ervoor te zorgen dat u niet zonder geld komt te zitten; het annificeren van een deel van uw bezittingen is dat wel. Het hele leven is niet de beste manier om met het tweede levensprobleem om te gaan; het goed structureren van pensioenen en lijfrentes is dat wel. Agenten voor het hele leven bedenken graag pensioenscenario's die u het gevoel geven dat u een permanente levensverzekering moet hebben of op zijn minst wilt hebben, vooral voor een getrouwd stel. Ze praten bijvoorbeeld over een pensioen dat pas wordt uitbetaald totdat de werkende echtgenoot is overleden. Of ze zullen praten over het annificeren van een deel van uw vermogen op basis van het leven van slechts één lid van het echtpaar. Dan zullen ze voorstellen dat de opbrengst van de hele levensverzekering wordt gebruikt voor de kosten van levensonderhoud door de tweede stervende echtgenoot. Er is geen reden om op deze manier een hele-levensbeleid te hanteren. Wilt u dat uw pensioen blijft lopen totdat u beiden overlijdt? Kies dan voor die optie. Als u wilt dat uw lijfrente loopt tot u beiden overlijdt, kies dan voor die optie. Ja, het wordt uitbetaald tegen een iets lager percentage, maar het verschil tussen de uitbetalingen is minder dan de kosten van een volledige levensverzekering die het verlies van dat pensioen zou dekken. Het is simpelweg niet de juiste oplossing voor het probleem. Biedt een volledige levensverzekering enige flexibiliteit bij pensionering? Zeker, maar de kosten voor die flexibiliteit zijn te hoog.

Het hele leven is niet de beste manier om dure spullen te kopen; daarvoor sparen is dat wel. Er zijn een aantal heel creatieve verzekeringsverkopers die pleiten voor systemen als Bank on Yourself of Infinite Banking. Het basisschema is als volgt:door uw polis op de juiste manier te structureren met gestorte bijtellingen, krijgt u in de beginjaren veel contante waarde in uw polis, zodat u in 3-4 jaar break-even draait in plaats van in 8-15 jaar. U koopt ook een polis die ‘niet-directe erkenning’ is. Dit betekent dat wanneer u van de polis leent, de verzekeringsmaatschappij dividenden blijft uitkeren over het bedrag dat erin zat voordat u het leende, zodat de polisdividenden in wezen de rentebetalingen op de lening tenietdoen. In plaats van naar uw spaarrekening of naar een bank te gaan om geld te lenen als u een auto, een koelkast of een vastgoedbelegging nodig heeft, leent u nu kosteloos van uw hele levenspolis. Bovendien zal de contante waarde van de polis die u niet leent sneller groeien dan het geld op een spaarbank.

Dus wat is het probleem? Het probleem is dat je een levenslange polis moet kopen die je niet nodig hebt. Het kan zijn dat u zelfs eerder failliet gaat dan met traditioneel beleid, maar er zijn nog steeds een aantal jaren met negatieve rendementen en op de lange termijn dezelfde lage rendementen. Is het beter om na 5 jaar 4%-5% per jaar te verdienen of vanaf jaar 1 1% per jaar te verdienen? Nou, de eerste 6 of 7 jaar ben je beter af met de spaarrekening van 1% per jaar. En als de rentetarieven vanaf hun historische dieptepunten stijgen, zit u nog steeds voor de rest van uw leven aan dit systeem vast. Nog niet zo lang geleden kon ik meer dan 5% uit een geldmarktfonds halen. Het lijkt ook heel eenvoudig om een auto bij een dealer te financieren tegen extreem lage rentetarieven. 0% of 1% is niet ongewoon. U kunt beter van hen lenen tegen 1% dan van uw polis tegen 5%. Het is een soortgelijk probleem met apparaten en hypotheken. Je doet al deze moeite zodat je van jezelf kunt lenen, en beseft dan dat het goedkoper is om van iemand anders te lenen. Als u ten slotte vijf of tien jaar lang geen aankoop hoeft te doen, heeft u de tijd om te investeren in iets dat waarschijnlijk een veel hoger rendement zal opleveren dan een levenslange polis. Worden degenen die erop vertrouwen dat ze worden opgelicht? Niet noodzakelijkerwijs, maar ze zijn over het algemeen oversold op de voordelen van hun plan. De voorstanders ervan zijn voornamelijk verzekeringsagenten die de omzet willen vergroten door middel van creatieve marketing. Sparen is simpelweg een betere manier om grote aankopen te doen dan een levensverzekering af te sluiten.

Voorstanders van het hele leven, vooral degenen die pleiten voor het gebruik van uw polis als bank, wijzen er graag op dat veel zeer rijke mensen en veel bedrijven (inclusief banken) feitelijk een volledige levensverzekering kopen. Hoewel het waar is, is het voor de gemiddelde persoon niet relevant. Grote bedrijven hebben geen toegang tot de belastingbesparende pensioenrekeningen die de middenklasse wel heeft. Ultrarijke individuen hebben deze al maximaal benut. Als u veel meer geld heeft dan u ooit nodig zult hebben, doet het rendement op uw geld er niet zoveel toe. Bill Gates kan het zich veroorloven om te investeren in iets dat een rendement oplevert van 2% tot 5%, omdat hij zijn geld niet nodig heeft om heel hard te werken. Dat geldt eenvoudigweg niet voor de overgrote meerderheid van de mensen uit de midden- en hogere klasse, inclusief artsen. Zoals hierboven besproken, hebben ultrarijke mensen ook meer baat bij de beperkte voordelen op het gebied van vermogensplanning en vermogensbescherming van permanente levensverzekeringen. Kortom, de lage rendementen die inherent zijn aan het hele leven zijn voor hen veel minder een probleem dan voor u.

Verkopers van het hele leven wijzen er graag op dat het hele leven een stuk goedkoper is als je het koopt als je jong bent. Hoewel het waar is dat de premies lager zijn als je een polis op 25-jarige leeftijd koopt dan wanneer je deze op 55-jarige leeftijd koopt, is het, als je eenmaal rekening houdt met de tijdswaarde van geld en het feit dat je de premies nog drie decennia lang betaalt, op jonge leeftijd geen betere investering dan op oudere leeftijd. Actuarissen zijn zeer intelligente mensen, en voor een risico dat relatief eenvoudig te modelleren is, zoals overlijden, kunnen ze de prijs van verzekeringen vrij efficiënt bepalen.

Naast de lagere premies zijn er nog twee redenen waarom het beter lijkt om deze op jonge leeftijd te kopen. Ten eerste wordt die commissie over meer jaren gespreid, waardoor deze minder impact heeft op uw totale rendement. Maar het alternatief om de commissie helemaal niet te betalen is veel aantrekkelijker. Ten tweede is het mogelijk dat u later in uw leven minder gezond wordt of een gevaarlijke sport gaat beoefenen. Dit is een van de ernstige nadelen van het gebruik van levensverzekeringen als belegging; niet iedereen kan er gebruik van maken. Ofwel komen ze er helemaal niet voor in aanmerking, ofwel is de prijs van de verzekering zo hoog dat het rendement op de investering zelfs lager is dan anders het geval zou zijn. Ik zie dat niet als een reden om het te kopen als je jong bent, ik zie het als een reden om het helemaal niet te kopen. Kunt u zich voorstellen dat Vanguard een paramedicus naar uw huis zou sturen om bloed af te nemen voordat u hun S&P 500-fonds zou kopen?

Een volledige levensverzekering is niet de beste manier om uw pensioeninkomen te beschermen tegen uw arbeidsongeschiktheid; een arbeidsongeschiktheidsverzekering is dat wel. Omdat ze beseften dat premies voor volledige levensverzekeringen erg duur zijn en moeilijk te betalen zijn in geval van arbeidsongeschiktheid, begonnen de verzekeringsmaatschappijen een polis aan te bieden die de premies kwijtscheldt in geval van arbeidsongeschiktheid. Soms lijkt het alsof u niet eens extra hoeft te betalen voor deze uitkering. Degenen die voor deze tactiek vallen, missen een paar punten. Ten eerste zijn garanties niet gratis. Elke garantie kost u geld in de vorm van een lager rendement, of de verzekeringsmaatschappij nu extra kosten in rekening brengt voor de garantie of dit “in de polis inbouwt” zodat het verborgen blijft.

Ten tweede is de arbeidsongeschiktheidsverzekering ingewikkeld en is de definitie van arbeidsongeschiktheid van groot belang. De meeste artsen die een arbeidsongeschiktheidsdekking willen, geven veel geld uit aan het krijgen van een hele mooie polis met een brede definitie van arbeidsongeschiktheid, inclusief dekking voor eigen beroep, omdat ze er zeker van willen zijn dat het bedrijf moet betalen in het geval van hun arbeidsongeschiktheid. De polissen die worden verkocht op basis van een levenslange polis zijn lang niet zo uitgebreid en de kans is veel kleiner dat ze worden betaald in de vele grijze gebieden waar handicaps vaak in vallen. U zult vrijwel zeker beter af zijn met het kopen van een grotere invaliditeitspolis dan een levenslange vrijstelling van premium rider. Uw arbeidsongeschiktheidsverzekering biedt mogelijk ook een pensioenbeschermingsrijder. Hoewel deze ook problemen met zich meebrengen (vooral wat betreft de manier waarop de uitkering wordt uitbetaald), zijn ze beter dan te proberen je arbeidsongeschiktheidsverzekering af te sluiten via een levenslange polis.

Als u, zoals ik, van plan bent vervroegd met pensioen te gaan, realiseert u zich misschien dat u uw arbeidsongeschiktheidsdekking sowieso niet nodig hebt om uw pensioenbijdragen te beschermen, tenminste na een paar jaar zwaar sparen. Overweeg om op 40-jarige leeftijd een portefeuille van €750.000 te hebben. U denkt dat u vandaag €2 miljoen nodig heeft voor uw pensioen. U bent van plan flink te gaan sparen, zodat u dat op uw vijftigste kunt bereiken en met pensioen kunt gaan. Wat is het back-upplan als u arbeidsongeschikt raakt en al dat geld niet kunt sparen? Uw arbeidsongeschiktheidsverzekering keert niet alleen uit tot 50 jaar. U betaalt ook tot 65 jaar. U hebt uw portefeuille dus niet nodig om die 15 jaar te dekken. U kunt ook beginnen met het ontvangen van socialezekerheidsuitkeringen tegen de tijd dat de invaliditeitsuitkeringen zijn afgelopen. Omdat u uw portefeuille niet hoeft aan te raken, kan deze blijven groeien. Als het na de inflatie met 5% groeit, zal het tegen de tijd dat je de leeftijd van 65 bereikt, in huidige dollars meer dan $2,5 miljoen waard zijn. Koop geen verzekeringen die u niet nodig heeft. Maar zelfs voordat u enige vorm van portefeuille heeft, is de beste manier om uw pensioensparen te beschermen het kopen van MEER arbeidsongeschiktheidsverzekeringen, en niet proberen deze uit een levenslange polis te halen. Zelfs als u de extra dekking zou kunnen gebruiken om uw pensioenportefeuille te onderhouden, moet u deze in een belegging met een hoog rendement kunnen stoppen, wat waarschijnlijk niet het hele leven zal opleveren. Een agressief belegde belastbare rekening is prima, aangezien uw hoofdinkomen als u arbeidsongeschikt bent, en uw arbeidsongeschiktheidsverzekeringsuitkeringen, belastingvrij zijn.

Aangezien een agent elke keer dat hij een nieuwe polis verkoopt een nieuwe commissie krijgt, zelfs als hij een oude van hetzelfde bedrijf vervangt, heeft hij een ernstig belangenconflict als hij u aanbevelingen doet. Ik heb op deze blog contact met veel verzekeringsagenten, en geen van hen is het met de anderen eens over wat een ‘goed gestructureerd’ levenslang beleid is. Dat betekent dat als u naar een tweede agent gaat, hij u vrijwel zeker zal vertellen dat er een betere manier is om het te doen. Wil het echter de moeite waard zijn om het ene beleid in te ruilen voor het andere, dan moet het oorspronkelijke beleid absoluut verschrikkelijk zijn, vooral na een paar decennia. De reden hiervoor is dat de slechte rendementen op levensverzekeringen zich vooral in de eerste jaren concentreren. Ik heb onlangs een polis bekeken. Dit is opgezet als een belegging met gestorte bijtellingen voor de eerste 25 jaar. Het was de beste poging van de agent om het rendement van een polis te maximaliseren. Zo zagen de rendementen op jaarbasis eruit:

Gegarandeerd Geprojecteerd Eerste 10 jaar-1,84%0,98%Volgende 15 jaar2,55%5,47%Volgende 25 jaar1,99%5,13%Dit toont aan dat de slechte rendementen zich in de eerste jaren sterk concentreren. Met deze specifieke polis neemt het rendement na 25 jaar zelfs af, omdat u dan stopt met premievrij bijbetalen. Bij een meer traditioneel beleid zou de derde rij iets hoger liggen dan de tweede rij. Maar de moraal van het verhaal is dat je eerst het ‘juiste beleid’ moet kopen, en zelfs een waardeloos beleid dat meer dan tien jaar oud is, zal beter zijn dan een geheel nieuw, beter beleid. Dit is ook de reden dat het een goed idee kan zijn om een polis voor het hele leven te behouden, zelfs als het kopen ervan in de eerste plaats een vergissing was. Het is ook opmerkelijk om te zien hoe weinig risico de verzekeringsmaatschappij feitelijk neemt, aangezien deze niet eens garandeert dat uw contante waarde gelijke tred houdt met de inflatie.

Het hele leven is niet de enige manier om bij uw overlijden geld belastingvrij door te geven aan uw erfgenamen. In feite is het niet eens de beste manier, een Roth IRA is dat wel. Als u overlijdt, krijgen uw erfgenamen een overlijdensuitkering die vrij is van inkomstenbelasting. Wat makelaars vaak niet vermelden, is dat vrijwel alles wat uw erfgenamen van u krijgen als u overlijdt, vrij van inkomstenbelasting is. Dankzij de verhoging van de basis bij overlijden wordt alles buiten een pensioenrekening, inclusief meubels, auto's, aandelen, contant geld, beleggingsfondsen en onroerend goed, allemaal geherwaardeerd op de dag van uw overlijden. Omdat de grondslag nu gelijk is aan de waarde, is er geen vermogenswinstbelasting verschuldigd. Het erven van een pensioenrekening kan nog beter zijn, vooral een Roth-rekening waarop de belastingen al zijn betaald. You can take all the money out the same year you inherit it and not pay any taxes at all. Or, you can “stretch it”, taking withdrawals gradually over decades until you die. Meanwhile, it continues to grow tax-free. You can stretch an inherited tax-deferred account too, but you do have to pay taxes on any money withdrawn from the account.

People invest in whole life insurance because they like guarantees. The insurance company guarantees that you'll get a certain rate of growth on your investment and it guarantees a death benefit. The guarantees, however, aren't worth nearly as much as people often assume. For instance, the guaranteed scale of any whole life insurance policy guarantees that your money will grow slower than the historical rate of inflation, despite sticking with it for half a century. Before deciding to trust a single company with your life savings, you might want to consider what happens if it goes out of business. There are state insurance guarantee associations that will cover the cash value and death benefit of your policy, but how much will they really cover? You might be surprised how little it is. In my state, only $500K in death benefit and $200K in cash value is covered, NO MATTER HOW MANY POLICIES YOU OWN. Your state is probably similar. No wonder agents are always talking about the long-term viability of their insurance company. It really does matter! Now I don't think the risk of any given insurance company going out of business in any given year is very high, nor do I think a typical purchaser is likely to end up with exactly the guaranteed growth rate. But before buying, you should realize that investing in whole life insurance isn't the risk free proposition agents like to present it as.

This one is pretty easy to see through, but you still see agents using it frequently. Since everyone “knows” that it is better to own a home than rent one, the agent says something like “You wouldn't rent your home for the rest of your life would you? So why would you rent your life insurance?” Basically, the agent is referring to the fact that if you use term insurance after age 60 or so, it becomes more and more expensive each year, just like renting a home. But unlike a home, you don't need life insurance after you become financially independent. When you only need a home for a year or two or three, it is a better idea to rent than to buy. When you only need life insurance for a decade or two or three, it is also a better idea to “rent” than to buy. The opportunity cost of “ownership” is simply too high.

This is a frequent one heard from the Bank on Yourself/Infinite Banking crowd. An underpinning of this school of thought is that the greedy banks are taking over the world so you should only do your financial work through the trustworthy insurance companies. To be honest, I don't have massive distrust for either one of these industries. Both industries have mutually-owned options (mutual life insurance companies and credit unions) where, like Vanguard, the customers own the company. The agents like to point out that banks actually own whole life insurance as part of their “Tier One Capital,” the money used to determine if the bank is adequately capitalized or not. This is somehow to make you fear that the banks know something you don't, like the financial world is about to implode and any of those using banks instead of insurance companies for their financial needs are going to go broke. Tier One Capital is a measure of a bank's financial strength. Banks use less than 25% of their Tier One Capital to buy single premium whole or universal life insurance on a group of employees. The bank owns the policy and is the beneficiary. When the employee keels over, the bank gets the cash. The bank is buying the policy primarily for the death benefit, not because the return is particularly high.

Tier One Capital is highly regulated and it is difficult for a bank to include riskier assets such as common stock(aside from that of the bank, which makes up most of Tier One Capital) and REITs in its Tier One Capital. When you are stuck choosing between low-risk/low-return investments, then you can understand why a bank might consider something like cash value life insurance with part of that money. However, individual physician investors investing for retirement have fewer restrictions on their investment options for their retirement. Most of them have significant need for their retirement money to grow. The returns available with cash value life insurance generally are not high enough for them to reach their goals. Even so, consider what a bank does with most of its Tier One Capital—it buys the only stock it can, it's own. If whole life insurance was so awesome, you'd think the bank would use all of its Tier One reserves to buy it. In short, doctors aren't banks, so doing what banks do isn't necessarily smart. Tier One Capital is highly regulated and it is difficult for a bank to include riskier assets such as common stock.

Agents, particularly of the Bank on Yourself type, love to point out that the golden parachutes for many highly-paid CEOs include cash value life insurance policies. However, just as the financial situation of a bank is dissimilar from that of a physician, so is the financial situation of a CEO making $10 Million a year different from that of a physician. When you're making a gazillion dollars a year, rate of return on your money becomes much less important and thus the benefits of whole life (asset protection, tax, estate planning, etc.) become relatively more important. It isn't that returns on whole life magically get better. Again, if you are in a position that you only need your long-term money to grow at 3%-5% nominal per year, then feel free to invest in whole life insurance. Most of us, however, need higher growth. Remember that a doctor making $200,000 per year and a CEO making $10 Million per year are in very different financial circumstances and what works fine for one will not necessarily work well for the other.

This myth again preys on the fears of a global economic meltdown. In 1933 there were two holidays. The first was a “Banking Holiday” in which the banks were closed for 10 days as sweeping regulatory changes took place. The second was an “Insurance Holiday” in which for a period of nearly six months you could neither surrender your cash value life insurance policies for cash, nor borrow against them. Aside from this holiday, 14% (63 companies) of life insurance companies actually DID fail during The Great Depression. In fact, if they would have actually marked to market the bonds and mortgages they held, they would have ALL been insolvent. Reforms were put in place during The Great Depression that fixed many of the problems leading to bank failures and the banking holiday. However, these reforms were never put in place for insurance companies.

This one usually goes like this. “If you can buy a bond yielding 5% and are in a 45% marginal tax bracket, the after-tax yield on that is just 2.75%. A whole life policy with a “tax-free” internal rate of return of 5% is better.” This is an apples to oranges comparison. What is the 1 year return on that whole life policy? 2.75% sounds a whole lot better to me than a -50%. Even at 10-20 years, the bond is still way ahead.

I wrote about a physician who was pleased with his 7% return on his whole life policy bought in 1983 (don't expect to see that again any time soon). Except that he could have bought a 30-year treasury that year yielding 10.5%. 10 years later, as his whole life policy is breaking even and interest rates have dropped, the bond purchaser has not only already more than doubled his money just from the coupon payments, but the capital gains on that bond added another 50% to his return. That investor would have done even better purchasing equities in 1983, the start of an 18 year bull market. A bond, which can be sold any day the market is open, simply cannot be compared in any fair manner to an insurance policy which must be held for life to have any decent kind of return. Besides, most physician investors can hold taxable bonds inside retirement accounts instead of a taxable account anyway. That retirement account not only provides for tax-protected growth like a whole life policy, but also a tax-rate arbitrage between your marginal rate at contribution and your effective rate at withdrawal, further boosting returns.

Even if your only choice is between buying bonds in a taxable account and buying whole life insurance, keep in mind that even at today's low interest rates you can still buy Vanguard's Long-Term Tax Exempt Muni Fund yielding 3.17% [2014] . The guaranteed return on whole life insurance cash value, held until your life expectancy, is about 2% and the projected return is only ~5%. Realistically, you should probably expect a return of 3%-4% over the long term on that policy. Of course, if you actually wish to cash out of that policy instead of borrowing from it (and paying interest for the right to borrow your own money), the earnings are just as taxable as any taxable bond fund. And if you want your money in a mere 10-20 years, you're going to come out way behind with the life insurance.

Now, if you really understand how whole life insurance works and you think its unique features outweigh its significant downsides, then feel free to run out and purchase as much as you like. It truly does not bother me. I do not make any money if you buy whole life, nor if you decide to buy something else. However, if you are like most, once you understand it, you won't buy it and in fact, if you already have, you'll probably be looking for the best way to get out of whole life insurance. Don't feel bad. 80% of those who purchase these policies surrender them prior to death, 36% within just five years. You've got to ask yourself why so many people who were apparently intending to hold this product for the next 40 or 50 years suddenly changed their mind. I'm sure it has nothing to do with it being inappropriately sold to the financially unsophisticated by insurance agents facing a terrible financial conflict of interest with their clients. Whole life insurance is a product made to be sold, not bought. It is a solution looking for a problem that exists for very few, if it exists at all.

This is one is merely misleading. The statement as it stands is true. The Free Application for Federal Student Aid (FAFSA) does NOT consider whole life insurance cash value as an asset of the student or the parents. The problem is, for the typical reader of this blog, that it doesn't matter. Your income alone will keep your child from qualifying for any need-based college financial aid. So if you buy a whole life policy for this reason, you're likely to be disappointed.

Another misleading argument. I'm always surprised to see people fall for this line, but they do. Do you complain when you don't get to use your car insurance for any given six month period? How about when your house doesn't burn down? Or you don't get cancer and get to use your health insurance? Then why in the world would you complain that your term life insurance expires and you're still alive. Term life insurance is pure insurance. If you die, it pays. If you live, it doesn't. As a general rule, since on average insurance must cost more than it pays out (since insurance companies have both expenses and profits), you should insure against financial catastrophes. When it comes to death, the financial catastrophe is dying during your earning years, before you become financially independent. So that's the only time period you need to insure against. Some people only fall halfway for this argument, and buy return of premium term life insurance. The same principle applies, of course. You don't walk away empty-handed when your term life policy expires. You had insurance for the entire term, which is exactly what you needed.

This outright lie comes from the true believers. They argue that whole life insurance is safe, liquid, tax-advantaged, creditor-proof, and offers a competitive return. These half-truths all add up to one big lie. Let's take them one at a time:

Safe from the cash value going down, perhaps, but not safe from losing money. A huge percentage of whole life insurance purchasers lose money because they cancel the policy at some point in the first 5-15 years before they break even on their “investment.”

I guess it's more liquid than owning a website or a rental property, but it pales in comparison to the liquidity available in a savings account or a mutual fund that can be liquidated any day the market is open. Even inside retirement accounts, there is absolute liquidity after age 59 1/2, and fair liquidity even prior to that date. Most of the time with whole life insurance you don't even get your money, you just have the right to borrow against it at pre-set terms. You can get that with a HELOC.

Few understand just how minor the tax advantages of whole life insurance are. There is no up-front deduction like a 401(k). Unlike a real investment, there are no capital gains rates if you surrender a policy with a gain and you cannot deduct the loss if you surrender it with a loss (the usual case). You don't get to use depreciation to reduce the tax burden of your income like with real estate. Instead of being able to withdraw the money tax-free like with a Roth IRA, you can only borrow against the policy, and that's tax-free but not interest-free, just like borrowing against your house, car, or mutual fund portfolio. Sure, you don't pay taxes on the “dividends,” but that's because they're actually a return of premium (i.e., you paid too much for the insurance). The only real tax break associated with life insurance is that the death benefit is tax-free. But that isn't any different from any other investment, where you get the step-up in basis at death. In addition, whole life can't be stretched like an IRA. The tax benefits, such as they are, are limited to a single generation.

Too few docs understand just how low the risk of needing this protection actually is. I calculate my risk of being successfully sued for an amount above policy limits at 1 in 10,000 per year. Maybe half that now that I'm practicing half-time. So should I be so unlucky as to be that one person, I would declare bankruptcy and be left only with protected assets. In my state, that's my retirement accounts, my spouse's assets, $40,000 in home equity, and whole life insurance cash value. Your state may or may not protect whole life insurance cash value. Please actually check if you are so paranoid to actually buy whole life insurance for this reason.

Are you kidding me? Competitive with what? Whole life insurance generally has a negative return for 5-15 years (sometimes more than 30 for really terrible policies). Even a good policy held for 5+ decades only guarantees a 2% return and projects a 5% return.

If I were going to draw up the perfect investment, it would definitely avoid the following characteristics of whole life insurance

It only qualifies as an “okay” investment in certain very limited situations. It's not even close to a perfect one.

This is one of my favorites to see in any sort of discussion with an insurance agent about the merits of whole life insurance. It usually comes when I point out that my problem with whole life insurance isn't so much the product as the way in which it is sold. Obviously, many of them take that quite personally since they've dedicated their life and career to selling this product inappropriately. So they point out that there are bad doctors or that insurance agents are just people trying to make a living. I don't have a problem with the sales profession. I don't even have a problem with people earning commissions for selling stuff. Cindy gets paid on commission to sell ads right here at The White Coat Investor. But if you seek advice from Cindy about whether buying an ad at The White Coat Investor is a good idea for you, you're a fool. Insurance agents are just people and people respond to incentives. An insurance agent has a huge incentive to sell you a whole life policy. The commission on a policy is 50%-110% of the first year's premium. Now you know why he's trying so hard to sell you a big fat doctor policy.

This was a new one to me. I thought I had heard every possible argument for buying a whole life policy until someone whipped this one out. How much trouble is it for you to deal with a 1099? It takes me about 30 seconds using Turbotax. Certainly not a reason to favor one investment over another. Remember not to let the tax tail wag the investment dog. Your goal isn't to minimize your taxes or maximize your tax-free income. It's to have the most money AFTER paying the taxes due.

Sometimes agents start with this argument, but frequently this is where they end, with ad hominem attacks. Sometimes it's phrased like one of these:

So, exactly how does being an ER doctor qualify you to give financial and insurance related advice?

Do everyone a favor and stick to studying medicine.

You’re young, a doctor and absolutely sure that you know everything.

Obviously, medicine has lots of problems and doctors don't know everything, but if the agent's best argument for whole life insurance is an ad hominem attack, that's a good sign that you should have stood up and walked out a long time ago.

This is the wrong question to be asking, but the answer to it is still no. Just because it is the only option presented to you by an insurance agent, doesn't mean it is the only option. Other options for retirement savings include defined benefit/cash balance plans, an individual 401(k) for self-employment income, a spousal Roth IRA, your spouse's employer-provided accounts, and Health Savings Accounts (HSAs). In some ways doing Roth conversions and paying off debt is also tax-sheltered. But most importantly, there is no limit on investing in a non-qualified mutual fund account (where long-term gains and qualified dividends are somewhat sheltered from taxes) or in real estate (where income is sheltered by depreciation and capital gains can be deferred indefinitely by exchanging).

Obviously investing in whole life insurance compares better to investing in a taxable account than to a retirement account (where there is no comparison from a tax, investing, or in most states an asset protection standpoint). But the real problem with this argument is that it is focused entirely on the idea that any tax-advantaged investment is always better than any fully taxable investment. That simply isn't true. It also mixes up the idea of an investment and an account, two things that financially naïve doctors sometimes have a hard time telling apart. (Think of the accounts as different types of luggage and the investments as different types of clothing.) The real question to ask yourself when you hear this argument is “Where should I invest after maxing out my available retirement accounts?” The answer is a taxable, non-qualified account. Now you're left with the question of what long-term investment to invest in—tax-efficient mutual funds, real estate, or whole life insurance? It's pretty hard to really compare the merits of those three investments and end up choosing whole life insurance given its limitations and terrible returns previously discussed.

The idea behind this argument is a rebuttal to the argument discussed in Myth #8. In summary, that argument is that you need whole life to avoid estate taxes, which is silly given the vast majority of doctors won't owe any federal estate taxes. The next step is for the agent to argue “Well, the estate tax exemption might be decreased.” Well, I suppose that's true. Congress can change any law they want any time they want. But buying insurance or investing based on what could happen seems foolhardy. I mean, it is probably just as likely that the estate tax is eliminated as the exemption reduced. It seems to me the best way to plan for the future is to project current law forward, since most laws aren't going to be significantly changed. If they are, you can make changes at that point. At any rate, it isn't like whole life insurance is some magic panacea to eliminate estate taxes. The only reason whole life insurance reduces your estate taxes is by making sure you have less money due to its low returns! The thing that reduces the size of your estate is the irrevocable trust you put the insurance into, and you don't even have to put insurance into it if you don't want to.

This one was particularly fun to debunk. Apparently, the idea here is to not pay for your own nursing home care somehow by purchasing whole life insurance instead of mutual funds. I'm not sure exactly how those envisioning this process think it will go. Maybe they think the nursing home doesn't ask for money until after you die or something, which is, of course, completely silly. But I think what they're referring to is the ability to spend down your assets to Medicaid levels, get Medicaid to pay for the nursing home, and still be able to leave a huge inheritance to your heirs because Medicaid somehow doesn't look at the value of your whole life insurance.

The whole process of Medicaid planning is a little distasteful to me to be honest. The idea is to hide someone's assets from the state so that the heirs can have them, foisting the cost of caring for the owner of those assets on to the public. But even assuming that you have no ethical problem with doing this, it's unlikely to work very well. Medicaid is state law, so it varies by state, but in Utah, a person can have up to $2,000 in countable assets and still qualify for Medicaid. Above that level, no Medicaid until you spend down to that level. If there is a spouse, the spouse can keep 100% of assets up to $24,720 and 50% of assets up to $123,600. Above that, Medicaid won't pay for the nursing home. Non-countable assets in Utah include:

So I guess if you want to hide money from Medicaid in Utah, then you could go buy a $1,000 whole life policy. Most states have similar policies regarding cash value life insurance. Even if there were a state with a higher limit than Utah, this seems silly for someone who should spend her entire retirement as a multimillionaire to be making plans to spend down to Medicaid levels for nursing home care. A far better plan to stiff your fellow Utah taxpayer (assuming you have a spouse who doesn't need care) is to upgrade your house and your car.

This statement has been made without explanation, but the idea isn't that complicated (nor misunderstood by WCI). You can borrow against the cash value in your whole life policy and use that money for whatever you want. You can spend it or you can invest it. Lots of whole life fans use fun phrases like “velocity of money” to describe buying a whole life policy, borrowing the money out, and investing it in something else. The really talented salesmen get you to invest it (along with any home equity they can get you to borrow out) in yet another insurance product.

Is there a cost to not maximally leveraging your life in this manner? Sure, anytime you can borrow at a lower rate and earn at a higher rate you'll come out ahead. But leverage works both ways, and the risk is not insignificant. What is not often mentioned by those advocating doing this is the opportunity cost of plunking money into a low return life insurance policy and buying unneeded death benefit instead of a higher returning investment. For instance, consider two options. You can invest $10K a year into an investment that returns 10% per year or you can buy a whole life policy that won't break even for 10 years. After 10 years, the first investment is worth $175K and the whole life policy only has a cash value of $100K. That's a $75K opportunity cost that apparently the “insurance agent doesn't understand.”

With a properly structured policy, you can break even in perhaps five years (maximizing the use of Paid-Up Additions), and using the combination of wash loans (interest rate to borrow against the policy =dividend rate of the policy) and a non-direct recognition policy, this idea becomes “not terrible.” You still have the opportunity cost of the first few years in the policy, but that is balanced out by a higher return on your cash in later years. I have discussed “Bank on Yourself” or “Infinite Banking” previously in detail if you are interested. It's not an insane use of whole life insurance, but it isn't for me. If you really understand how it works (it's going to take working through a lot of hype to do so) and want to do it, go for it.

In recent years, insurance companies are adding on a Long Term Care rider to whole life insurance policies (and universal life policies and annuities) and agents are using the fear of expensive long term care to sell them. I find this appalling. Not only are you mixing insurance and investing, but you're now combining two different types of insurance policies with investing. Given the track record of insurance companies with long term care, I think most of my readers should strive to get a place where they can self-insure the risk of long term care, but even if they cannot, I'd prefer a simpler long term care policy on its own than mixing it with an otherwise unnecessary and expensive insurance policy.

The benefit of buying this as a rider of a whole life policy is that the premiums of the policy are guaranteed—you don't have the risk of the insurer upping the premiums like you do with a long term care policy or upping the cost of the underlying insurance like you do with a universal life policy. Those guarantees are worth something.

Remember we're not talking about just an accelerated death benefit. This is just another way of self-insuring long-term care, but with a lower return on the investments used to pay for it. You're really buying two policies combined into one. But there's no free lunch here. You're either paying more for the combined policy, or you're getting less of something, usually death benefit. Most likely, you're also paying for a life insurance policy you don't need or wouldn't otherwise buy. That death benefit isn't free. The reason life insurance companies stopped selling long term care insurance and started selling these hybrid policies is that their actuaries were convinced they are more likely to make money that way. That profit has to come from you, there is no other possible source.

If you do decide you wish to purchase some sort of long term care insurance policy, it is entirely possible that a hybrid product is right for you, but just like health and disability insurance, the devil is in the details. Read the fine print and be sure you know what guarantees the insurance company is actually providing. Know about what is covered, what isn't covered, and whether benefits are indexed to inflation or capped. Or better yet, live like a resident for 2-5 years out of residency so you'll be rich enough to self-insure this risk and never have to make this decision.

This argument is simply bizarre, but used by agents once the prospective buyer has refused to buy the massive policy they were offered at first. A small commission is better than no commission, I guess. Of course, you shouldn't put all your money into whole life insurance, that's a straw man argument. Also, if buying a policy is a bad idea, you're going to be better off if you buy a small one than a big one. But that's hardly a reason to buy a policy in the first place. Like any asset class, if it isn't a good idea to put a significant chunk of your portfolio into it, it probably isn't a good idea to put any of your money into it.

This argument is used when I point out that literally hundreds or even thousands of my readers have been sold clearly inappropriate insurance policies. The problem is there are two options to explain this phenomenon. The first is that these agents are unethical. The second is that they're incompetent. Given the statistic that 80% of policies are surrendered prior to death and 76% of the docs I've surveyed regret their purchase, this is hardly just a “Few Bad Eggs” doing this. It's an industry-wide problem.

This one is used to sell insurance to people that don't even have a need for insurance. The idea is to prey upon their fear of the combined risk of needing insurance AND not being able to purchase it. One example would be a 25-year-old single doc with no kids. No life insurance need here. “But what if you get diabetes before you get married and have kids? You should buy the policy now.” Uhhhh . . .no.

First, you may never have dependents.

Second, if you do need it, you'll probably be able to buy it at that time at a reasonable price.

Third, if you do become less insurable, you will still likely have options for some insurance through an employer or other groups.

Fourth, even if you become uninsurable through anyone, the risks must be multiplied. For example, let's say there's a 5% risk of you becoming uninsurable before you have a real insurance need. And the risk of you dying before reaching financial independence is 5%. To get your true risk of a financial catastrophe, you must multiple those risks. 5% x 5% =0.25%. That is a 1 in 400 chance. Life is risky. You can't eliminate every possibility of something bad happening to you and even if you could, that wouldn't be a wise use of your money. Wait to buy insurance until you have a need for that insurance.

This argument is often even extended to children. If you're buying life insurance from the same company that sells you baby food, you're probably doing something wrong. Now, if you could buy a lot of future insurability for that kid very, very cheaply, that might be something to consider. Unfortunately, you can't really do that for several reasons:

First, you have to actually buy unneeded insurance. That newborn likely won't have any need at all for life insurance for 25-30 years.

Second, you're not pre-buying the policy that kid will need. You can't buy the right to buy a 30-year level term policy at age 30. You have to buy a whole life insurance policy. Which means you're also paying for insurance that will be unnecessary on the far end of life too, after the kid has become financially independent.

Third, you generally can't buy enough insurance, or even enough future insurability, to actually meet any sort of realistic life insurance need. Most of these infant policies are only $10K or so. That's basically a burial policy, and as sad as it would be to bury your kid, it's not a financial risk my readers should need to insure against. (I've even heard the argument that you should buy the policy so you can take a few months off work because you'll be too distraught to work, but that's what an emergency fund is for.) Even if you find a policy that allows you to purchase future insurability for a larger policy, let's say $500K, that's not going to mean much in 30 years when the life insurance need actually shows up for the first time, much less in 50 years when the kid is actually reasonably likely to die. At 3% inflation, $500K today will only be worth $200K in 30 years and $109K in 50 years. Better than nothing, but you went to all this effort and expense to preserve insurability and your kid still ended up with inadequate life insurance coverage.

I had this one pitched to me by a doc turned financial advisor of all people. The argument was that you could buy whole life with pre-tax dollars and then if you wanted to pull the policy out of the defined benefit plan you could do so. He felt this was an “advanced technique” for “high net worth folks.” I was flabbergasted. It was such a stupid idea I couldn't believe it. A defined benefit/cash balance plan already provides tax protected growth and asset protection, two reasons frequently cited to buy whole life insurance. You're now paying twice for those benefits. To make matters worse, should you die while this policy is in the defined benefit plan, part of the death benefit becomes taxable, negating another usual advantage of life insurance—a completely tax-free death benefit. But the main reason why this is such a stupid idea is when it comes time to close the defined benefit plan, which is usually done every 5-10 years or so in order to roll it into an IRA. At that point, you have to do one of two things.

First, you can surrender the policy and move the cash surrender value into the IRA. But what is the investment return on the first 5-10 years of a whole life policy? You break even if you're lucky. Not exactly a great investment for that time period, especially compared to a typical conservative mix of stocks and bonds.

Second, you can purchase the policy from the plan. Of course, you have to do that with AFTER-TAX dollars. So while you initially bought it with the pre-tax dollars in the plan, eventually you're going to have to cough up after-tax dollars for the policy. And then what are you left with? A whole life policy you probably neither want nor need and perhaps even with associated premiums you have to make each year. Some deal!

This myth showed up in a comment on a post on this blog. I thought it was particularly creative, especially with the way it was combined with Myth #8 (You Need Whole Life to Help For Estate Planning) and Myth #25 (Term Life Expires Without Paying Anything):

More money is passed through life insurance than any other way. I’ve seen too many people out live term which is throwing money away and need life insurance and are at that time in life uninsurable. Life is really used well in estate and trust planning.

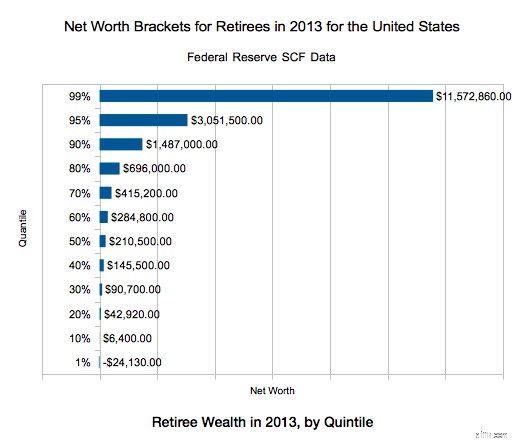

Surprisingly, this was the first time I had heard this argument. Being financially literate, of course I was able to immediately debunk it, but I suppose somebody might fall for it. There are two problems with this statement. First, it may not even be true. I looked and looked and looked for a study that showed what assets are actually inherited, without finding anything that actually quantified it. So if there is a study that actually says this, I suspect it is paid for by a life insurance company. Maybe it's true, maybe it's not, but I suspect it isn't given how few people have life insurance in force at their death. I suspect more money is left behind in houses than anything else. I mean, look at the net worth of people by age. Among retirees, the 50th percentile for net worth is $210K. That's got to be mostly house. The 80th percentile is $696K. That's about the average price of a house in my upper middle class neighborhood in a flyover state.

That jives with the average estate left behind at death:

It seems very unlikely that the main inheritance most people receive is the proceeds of a life insurance policy given those numbers. How many retirees even carry life insurance? According to this, about 65% of those 65+. But 47% of those own less than $100K of life insurance. It is a well known statistic that fewer than 1% of term life insurance policies pay out. It isn't that the insurance companies aren't good for the money, it's just that people out live the term. A lesser known statistic is that 80%-90% of whole life insurance policies don't pay out either. They're surrendered prior to death, often at a loss since 1/3 of policies are surrendered in the first 5 years and over half in the first 10 years.

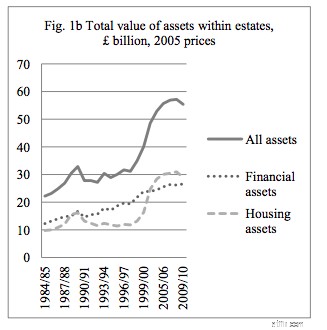

I did manage to find some UK data, however, which suggests my hunch (that people inherit more in real estate than life insurance proceeds) is correct.

As you can see, more than half of inherited assets are housing assets, so clearly more assets cannot be passed as life insurance than anything else.

Perhaps the agent wasn't referring to the median inheritance though. Perhaps he was referring to the total amount of dollars passed to heirs. I could find no data to support nor refute that notion.

Second, even if the statement is true, it is irrelevant. Given that THE PURPOSE of life insurance is to pass assets on to heirs, that's hardly an argument to buy life insurance for some reason besides the death benefit. As I've always said, if you want a life long death benefit that gradually increases throughout your life, then a whole life insurance policy is a great way to get that (although a guaranteed universal life policy can provide a level life long death benefit at about half the price and is probably a better solution for those who really need a permanent death benefit). Bear in mind that you are likely to leave a larger inheritance by investing in stocks and real estate than buying life insurance due to the higher returns, and those assets, just like life insurance, provide a tax-free inheritance to your heirs. Life insurance only provides a larger inheritance if you die well before your life expectancy.

This one confuses a lot of people and they get really mad when they realize how whole life insurance works. They mistakenly believe that they get a death benefit for their heirs AND a separate “cash value” investment type account that they can use themselves or leave for their heirs. What they do not realize is these two pots of money are one and the same. That which you use for yourself does not get passed on to your heirs. When they discover this fact, they feel like the insurance company is stealing a bunch of money from them and their heirs.

In reality, when you borrow against your life insurance policy, you are borrowing against your death benefit. When you die, your heirs get the death benefit minus any outstanding loans. The amount of the outstanding loans, of course, can never be more than the cash surrender value of the policy, which gradually grows to an amount very close to the death benefit at your life expectancy. So really the cash value just tells you how much of the death benefit you can borrow at any time. You can either borrow this pot of money (death benefit/cash value/surrender value) and spend it yourself, surrender the policy and spend the money, die and leave the money to your heirs, or some combination of the above. But there isn't two pots of money. There isn't a $400K cash value and a $1M death benefit. There is just a $1M death benefit. If you spend $400K of it, your heirs only get $600K of it. So you don't get an investment AND life insurance, you get an investment OR life insurance.

Daar ga je. Forty reasons for buying whole life insurance debunked. Maak je geen zorgen; the agents who sell this stuff will come up with more. Just hang out in the comments section over the next year or two and you can watch. Whole life insurance is a product designed to be sold, not bought and the only way to win an argument with an agent trying to sell it to you is to stand up and walk away. As Upton Sinclair famously said, “It is difficult to get a man to understand something, when his salary depends on his not understanding it.” Maybe it should be called Whole LIE Insurance.

Whole life insurance is a terrible investment if you don't hold on to it to your death. Since the vast majority of people surrender their policies prior to death, it is a terrible investment for the vast majority of those who purchase it. If you want to invest in it, then you need to place a very high value on its unique aspects and not mind it's serious downsides.

The ideal purchaser of whole life insurance should:

The fact is that only a tiny percentage of the population, far smaller than the number of people who have been sold these policies historically, meets all or even most of these criteria. Whole life insurance remains a product designed to be sold, not bought.

Heeft u meer vragen over levensverzekeringen en welke polissen het beste bij u passen? Huur een door de WCI goedgekeurde professional in om u te helpen dit probleem op te lossen.

Agree? Disagree? Please reference which “myth” you're referring to in your comment and keep comments civil and on topic. Ad hominem attacks will be deleted.

[This updated post was originally published as a series from 2013-2019.]

De White Coat Investor kan een vergoeding ontvangen van White Coat Insurance Services, LLC; gelicentieerd in alle staten, inclusief MA en DC; CA-licentie #6009217; NY-licentie #1758759 (exp. 6/2027); Geregistreerd adres:10610 S. Jordan Gateway, #200 South Jordan, UT 84095. Dit heeft geen invloed op de kosten of dekking van de verzekering.

Wat de nieuwste Covid-19-hulpwet betekent voor uw kleine bedrijf

Wat is een reeds bestaande aandoening?

Budgettaire doelen om variabel inkomen te motiveren

American Express Membership Rewards® Review

In aanmerking komen voor welzijn in Massachusetts

Hoe u met een beperkt budget werkt:de essentie

Een filiaalnummer vinden op een cheque